E‑commerce in India is a rapidly expanding digital retail sector that connects millions of consumers with local and global sellers through online platforms, mobile apps, and social channels. As of 2025, the market is projected to exceed $180 billion in Gross Merchandise Value (GMV), driven by a young, mobile‑first population and a surge in digital payment adoption.

- Internet penetration now tops 70 % and continues to climb.

- Unified Payments Interface (UPI) processes over 10 billion transactions per month.

- Logistics firms are cutting average delivery times to under 48 hours in major metros.

- Regulatory reforms, such as relaxed FDI caps, make foreign investment easier.

- Consumer confidence is rising, but price sensitivity and returns handling remain challenges.

Market Size and Growth Trajectory

India’s e‑commerce GMV grew from $84 billion in 2020 to $180 billion in 2025, a compound annual growth rate (CAGR) of about 19 %. The surge is fueled by three main forces:

- Demographic dividend: Over 600 million people are under 35, and 55 % own smartphones.

- Improved connectivity: 4G coverage is now nationwide; 5G trials are underway, promising faster load times and richer media.

- Trust in online transactions: Payment successes and robust return policies have shifted consumer mindsets.

Category‑level growth shows fashion and electronics leading the pack, while groceries and health‑care have seen the fastest percentage rises thanks to pandemic‑induced habit changes.

Infrastructure Readiness: Internet and Mobile

The backbone of any e‑commerce ecosystem is reliable internet. According to the Telecom Regulatory Authority of India (TRAI), broadband subscriptions crossed 350 million in early 2025, with average speeds of 120 Mbps on urban fiber networks. Rural broadband, powered by the BharatNet project, now reaches 75 % of villages, narrowing the digital divide.

Mobile internet dominates: 450 million active 4G users and an estimated 200 million 5G‑ready devices slated for rollout by the end of 2025. This mobile‑first reality means platforms must prioritize responsive design, lightweight pages, and progressive web apps (PWAs) to capture users on slower connections.

Payment Landscape: From Cash to UPI

Digital payments have moved from a niche offering to the main transaction method. The Unified Payments Interface (UPI) alone recorded 10.5 billion transactions in Q2 2025, amounting to over $120 billion in value.

| Method | Share of Transactions | Growth YoY |

|---|---|---|

| UPI | 55 % | +23 % |

| Credit/Debit Cards | 30 % | +8 % |

| Digital Wallets (Paytm, PhonePe) | 12 % | +5 % |

| Cash on Delivery (COD) | 3 % | -10 % |

Bank‑linked payments are tempting because they reduce fraud risk and improve cash flow for sellers. However, COD still exists in tier‑2 and tier‑3 cities, where trust in online payments lags behind.

Logistics and Delivery Networks

India’s logistics sector has transformed thanks to major players like Delhivery, Ekart, and Ecom Express. Average delivery windows in metros have shrunk from 5‑7 days (2020) to 1‑2 days for many SKUs. In smaller cities, the average is now 3‑4 days, a dramatic improvement over the past half‑decade.

Key logistics enablers include:

- Warehouse automation: AI‑driven inventory management reduces stock‑outs by 15 %.

- Micro‑fulfilment hubs: 1,200+ satellite centers bring products within a 50‑km radius of consumers.

- Hyperlocal delivery startups (e.g., Dunzo, Swiggy Instamart) that handle low‑value, high‑frequency orders.

Despite progress, last‑mile challenges remain in remote areas, where road quality and address verification can add 2‑3 extra days.

Regulatory Environment and Policy Support

Government policies have become more e‑commerce friendly. The 2024 amendment to the Foreign Direct Investment (FDI) rules lifted the cap on e‑commerce marketplace investments from 49 % to 100 % for entities that do not hold inventory. This encourages global giants to set up wholly owned subsidiaries.

Other supportive measures include:

- GST simplification: Uniform 5‑% GST on e‑commerce services reduces compliance friction.

- Data localisation guidelines that ensure consumer data stays within Indian borders, boosting trust.

- Initiatives like the “Digital India” mission, which subsidises broadband for small retailers.

On the flip side, the government is tightening rules around “unfair trade practices,” requiring platforms to disclose seller ratings and product origins more transparently.

Consumer Behaviour Trends

Indian shoppers are experimenting more with new categories. A 2025 Nielsen report shows:

- 70 % of respondents have bought clothing online at least once.

- 45 % have purchased groceries via an app, up from 28 % in 2022.

- Average basket size has risen to ₹2,500, reflecting higher disposable income among the middle class.

Key motivations include price comparisons, convenience, and a growing appetite for international brands. However, concerns around fake products and return hassles still deter a segment of the market.

Opportunities and Challenges for New Entrants

If you’re thinking of launching an e‑commerce venture in India, here’s a snapshot of the playing field:

| Opportunity | Challenge |

|---|---|

| Massive, untapped tier‑2/3 consumer base | Logistics and address verification difficulties |

| Robust digital‑payment ecosystem (UPI) | Regulatory compliance for data localisation |

| Government incentives for MSME digitisation | Intense competition from established marketplaces |

| Rise of social commerce via Instagram, WhatsApp | High customer acquisition costs in saturated categories |

Success hinges on niche selection, seamless mobile experience, and a logistics partner that can guarantee fast, reliable delivery.

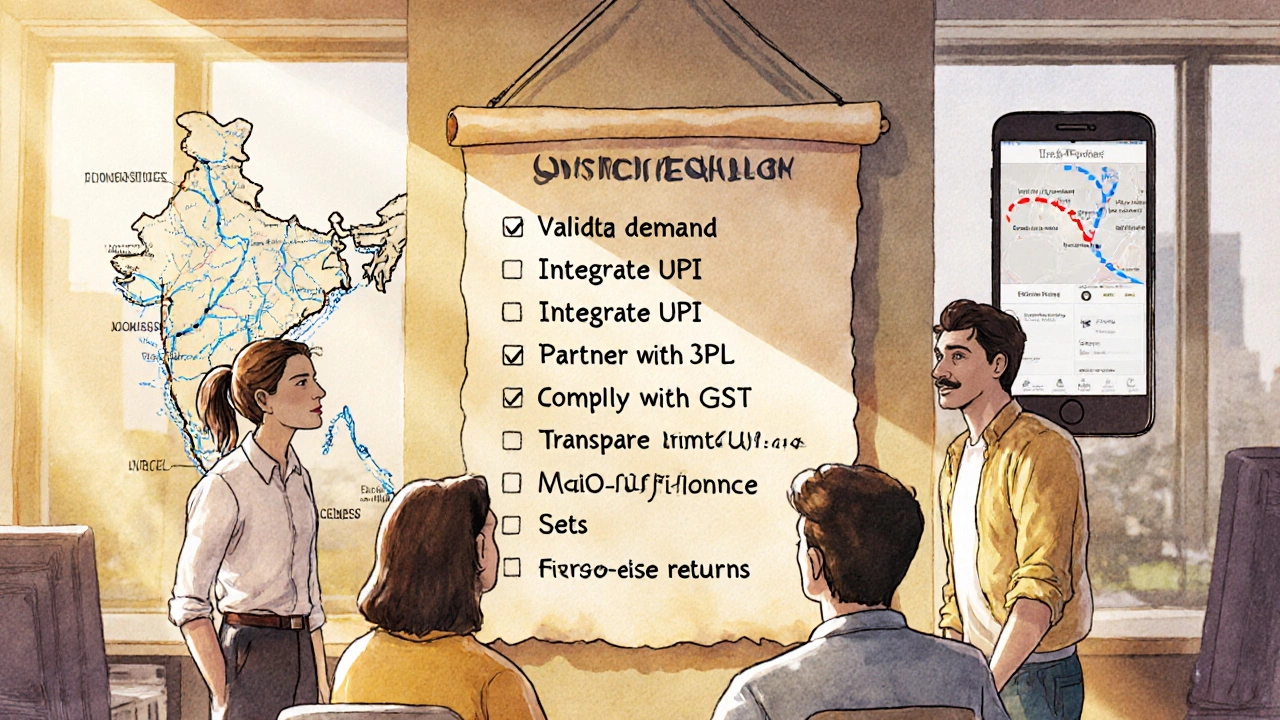

Quick Checklist for Entrepreneurs

- Validate demand with a minimum viable product (MVP) targeted at a specific region.

- Integrate UPI, credit‑card gateway, and one digital wallet before launch.

- Partner with a 3PL that offers COD handling if you serve tier‑2 cities.

- Ensure compliance with GST, data‑localisation, and marketplace‑seller policy.

- Invest in mobile‑first UI/UX; load times under 2 seconds are critical.

- Set up a transparent returns policy to build trust.

Frequently Asked Questions

Is the Indian market still growing or has it plateaued?

Growth remains strong. The sector is projected to hit $250 billion in GMV by 2030, driven by rising internet users and expanding payment options.

Do I need to set up a local entity to sell in India?

Yes. Foreign sellers must register a legal entity (LLP or Private Ltd) to comply with GST and FDI regulations.

How important is COD in 2025?

COD now accounts for just 3 % of online transactions, down from 30 % in 2020. It’s still relevant in smaller towns but can be phased out in metro‑centric models.

What logistics partner should I choose?

Pick a partner that offers both national reach and micro‑fulfilment hubs. Delhivery and Ekart are popular for mid‑size sellers; hyperlocal startups work well for low‑value, high‑frequency items.

Are there any upcoming regulations I should watch?

The government plans stricter disclosure rules for marketplace listings in 2026 and is reviewing the e‑signature framework for faster onboarding.